Case Study: How Amazon killed the Bookstore

One of the best ways I learned how to identify great companies was to study a handful of successful companies, how they started, how they disrupted large incumbents, continued to grow, and fended off disruptors once they became the dominant force. To do this, I looked at both qualitative and quantitative characteristics, what were they doing during periods of large share price growth and decline?

Once I did a couple of these, it became clear to me great companies had many common traits. I was then able to look for these traits in companies that were earlier in the lifecycle. Here is an example of the case study I did on Amazon.

Note: everything written below is my own opinion and analysis and is not meant to be taken as financial advice.

Disclaimer: I am not an Amazon shareholder, but I am an Amazon Prime subscriber :)

The rise of Amazon and the three things customers care about [1994 – 2004]

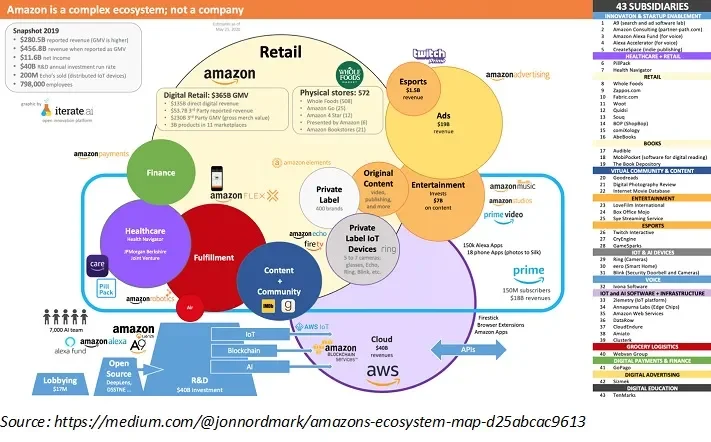

Amazon started by selling books. Today it generates $575bn in revenue and runs 40% of the world's cloud infrastructure. This is the playbook — how a company built around three simple customer promises created the most valuable ecosystem in business.

Jeff Bezos founded Amazon in 1994 as an online book retailer. But he never thought of it as a book company — books were just the starting point.

Amazon's core strategy focused on customer obsession. After extensive research, Amazon found that customers cared most about three things when shopping online:

After extensive research, Amazon found that customers cared most about three core features when shopping online:

A large selection of products

Low or competitive prices

Seamless delivery and returns.

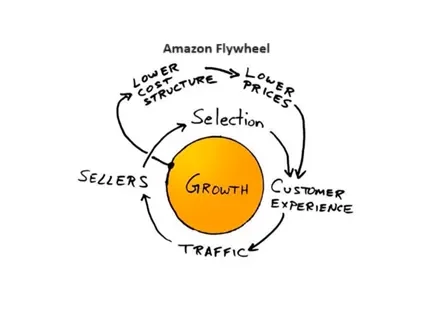

Rather than focusing on margins and profitability in its early years, Amazon's sole purpose was to deliver on these three features and fundamentally change how consumers felt about online shopping. We include the Amazon flywheel below:

Why books were the perfect wedge

Bezos created a list of roughly 20 products that could benefit from online marketing and narrowed it to compact discs, computer hardware, software, videos, and books. The defining feature: each product had to be homogenised. Consumers had to be sure of what they were purchasing, making price the primary decision driver.

Books won because the category had many titles but only a handful of distributors to negotiate with. More importantly, Amazon's lower cost structure as an online retailer meant it could carry a vastly larger selection without floor space restrictions.

By 1997, Amazon carried more than 2.5 million book titles. A local bookstore had a fraction of that.

The result was astronomical. Customers no longer needed to visit a store. They could choose from an almost unlimited selection with a few clicks at a lower price, and the return policy was easy. Sales soared as more people discovered this new way to shop.

Amazon was trying to change shopping behaviour that was ingrained for years. It had to start small, and books were the perfect product: homogenised, widely demanded, and easy to ship.

Customer reviews emerged from the growing user base, creating a network effect. Hundreds of reviews per product meant shoppers could buy with confidence. Each new customer made the platform more valuable for every other customer.

What Amazon looked like as an investment?

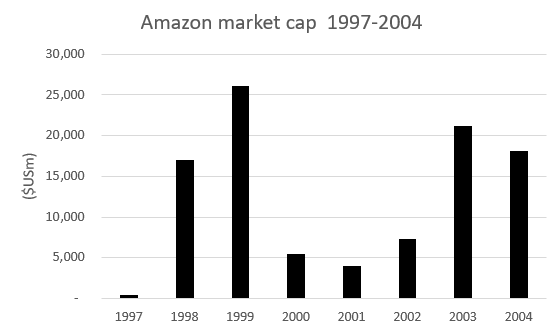

Amazon IPO'd in 1997 at a valuation of roughly $438 million. By 1999, the valuation had reached over $30 billion.

Then the tech wreck hit. Amazon's valuation fell 90%, from $30 billion to roughly $2 billion.

This is a critical lesson: no matter how great a company is, it is not immune to market cycles. For owners of Amazon stock who purchased near the peak, it took until 2007 before the valuation recovered. The timing of your investment matters.

Right before the crash, Amazon sold roughly $700 million in convertible bonds, a move that gave it the capital to survive while many competitors folded. Without that raise, Amazon could look very different today.

Why valuation doesn’t always reflect fundamentals in the short term.

I see similarities between the tech wreck and the recent tech boom and bust. Let me illustrate with an example.

Imagine I opened a cafe with amazing coffee, clearly better than Starbucks. My business has taken off, I've opened 50 cafes with plans to make that 5,000 in three years. I'm valued like a superstar growth company.

Then the environment changes. Interest rates rise. Capital becomes expensive. Funding dries up.

I've committed all my money to opening the fanciest stores and paying top dollar for staff. I no longer have access to capital. I can't hire the best baristas or open cafes in the best locations. Meanwhile, Starbucks has the financial flexibility to keep investing.

Despite seemingly being the same company, my valuation plummets, because due to macroeconomic factors, I can no longer fund the same growth algorithm. I can no longer execute my strategy and now a fundamentally different company despite day to day operations hardly changing. Market sentiment, positioning, environment, and macro conditions do matter.

Some companies in the recent cycle reached valuations on very high multiples based on future growth prospects that subsequently fell apart. In that specific environment, some of those valuations may have been justified, which is one reason bubbles always fool us.

Key takeaway from the early years

Amazon solved a real problem and genuinely improved the consumer experience. It had one primary focus: customer obsession, and built its entire strategy around that ethos.

As the challenger, Amazon allocated resources to where it could provide a differentiated service, using its lower cost structure to offer more selection at lower prices. The flywheel started spinning.

In Part 2, I'll cover how Amazon evolved from an online bookstore into a global ecosystem through Prime, the marketplace strategy that beat eBay, and AWS.

How Amazon became everything - Global Dominance [2004-Present]

In Part 1, I covered how Amazon used customer obsession and a lower cost structure to disrupt book retail. This part covers the three strategic moves that turned Amazon from an online store into an ecosystem worth $1.3 trillion: Prime, the open marketplace, and AWS.

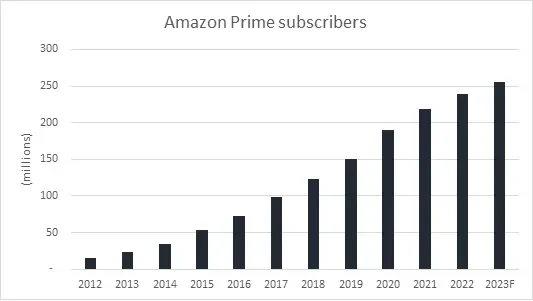

Amazon Prime — the subscription that changed everything

Amazon knew that fast, seamless delivery was essential for e-commerce to beat traditional retail. But shipping costs were a barrier, especially for everyday household goods.

Amazon Prime was born. Launched in 2005, customers paid $79 upfront for unlimited two-day delivery, compared to $9.48 per shipment. The addressable market expanded immediately as shoppers became willing to buy everyday goods online.

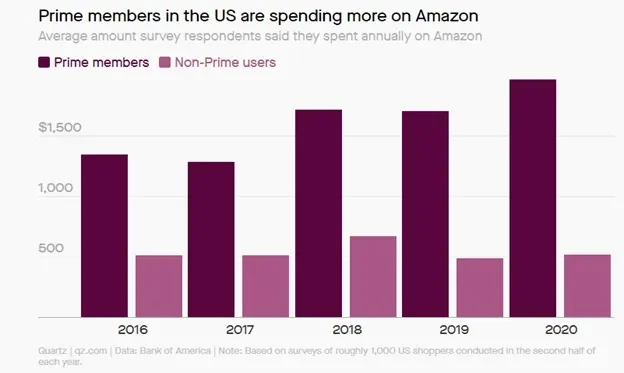

Prime members spend approximately four times more than non-Prime members, driven by both frequency and average basket size.

Prime has since surpassed 230 million subscribers, generating roughly 7% of Amazon's revenue and growing. But the genius of Prime goes beyond shipping.

Prime evolved into an entertainment platform, adding Prime Video, Prime Gaming, Prime Music, and Prime Reading. This created a flywheel within a flywheel: revenue from subscribers who signed up for free shipping funds media content, which drives further subscriber growth, which drives more e-commerce purchases.

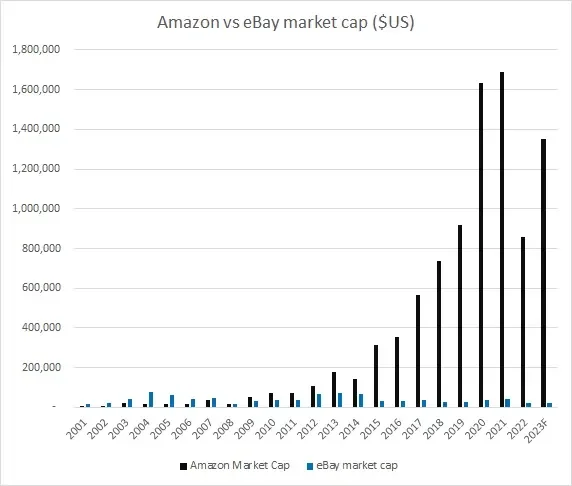

The open ecosystem and why Amazon beat eBay

This is, in my view, one of the most important strategic decisions Amazon ever made.

Amazon could have used its competitive advantages to eliminate competitors. Instead, it opened its ecosystem. It expanded from an online store into an online marketplace, allowing other vendors to sell products on the platform and use Amazon's supply chain and delivery services.

Think about what this meant: rather than solely benefiting from its supply chain as a competitive weapon, Amazon let other retailers use that same infrastructure. Competitors became partners. The product catalogue exploded.

It is much harder to displace an ecosystem than a company. Amazon turned competitors into customers.

The strategic difference with eBay is critical. eBay is seller-focused. It treats the seller as its primary customer. The site is built around seller stores, with reviews based on the seller. Amazon is product-focused, search functionality centres on products with multiple sellers at different price points, and reviews focus on the product itself.

While eBay may be preferred by sellers looking to establish their own brand, Amazon proved to be the better platform for customers. Third-party services now contribute roughly 24% of Amazon's total revenue.

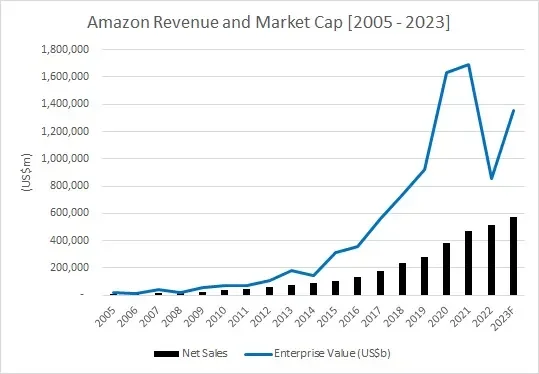

For context: in 2004, eBay was worth nearly $33 billion while Amazon was worth $18 billion. Today, eBay is worth roughly $25 billion (after spinning off PayPal). Amazon is worth $1.3 trillion.

AWS: Sharing the infrastructure

Amazon Web Services follows the same open ecosystem logic. As Amazon scaled, it had to build internal computing infrastructure to handle its hyper-growth. That infrastructure became so good that Amazon began selling it to other businesses.

Businesses could rent compute power, storage, servers, and networking on a pay-as-you-go basis. AWS solved a real problem, companies could outsource their IT infrastructure instead of building and managing it themselves.

AWS now generates roughly 16% of Amazon's revenue at $91 billion, with significantly higher margins than the retail business. It's the profit engine that funds everything else.

The financial profile

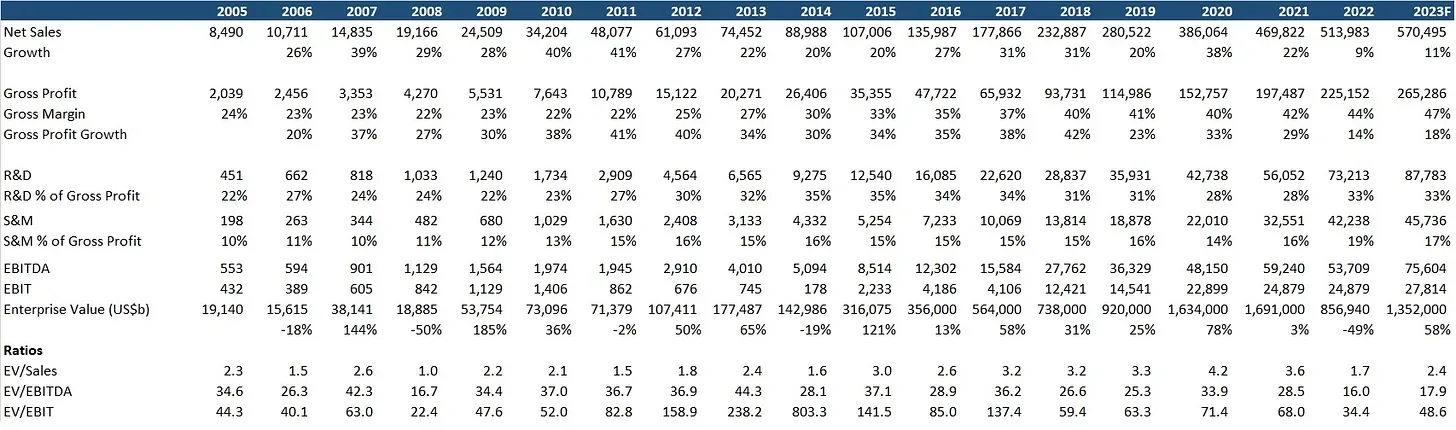

Amazon averaged 27% revenue growth annually from 2005 to 2023. That's almost two decades of 20%+ growth at massive scale, downright ridiculous.

During this period, gross margins improved from 20% to roughly 47% today. Amazon consistently invested 20-30% of gross profit into R&D and 10-20% into sales and marketing. Instead of scaling back spending to take profits, Amazon improved profitability through efficiency and scale.

Investors will reward investment if it is backed up by revenue growth. If Amazon ever chose to completely scale back investment, it would be a significant cash-generating business.

Once Amazon reached critical mass, it used its financial power for acquisitions: Whole Foods ($13.7bn) for grocery, MGM ($8.5bn) for Prime Video content, One Medical ($3.9bn) for healthcare, and Twitch ($970m) for gaming. Each acquisition expanded the ecosystem, entering new markets, unlocking cross-sell synergies, and strengthening the flywheel.

While Amazon's enterprise value skyrocketed, it achieved consistent annual earnings growth, meaning multiples remained somewhat consistent. This just goes to show that as long as you can achieve consistently strong revenue growth, investors will reward investment.

As Amazon grew, it earned investors' trust, essentially unlocking an unlimited supply of capital. Amazon could test other ideas at relatively low risk compared to other companies. Once Amazon reached critical mass, it flexed its financial power to continue growing through acquisitions. I want to highlight Amazon's top five acquisitions:

Whole Foods (US$13.7bn, 2017) – Dramatically expanded Amazon's brick-and-mortar footprint and gave Amazon a much stronger position in grocery deliveries.

Metro-Goldwyn-Mayer (MGM) (US$8.5bn, 2021) – American media company specialising in film and television production to grow Prime Video.

One Medical (US$3.9bn, 2022) – As Amazon looks to grow its healthcare operations

iRobot ($1.4bn, 2022) – Amazon expands its automated robotic devices (Roomba!)

Zappos $1.2bn, 2009) – An online shoe and clothing retailer, acquired to expand Amazon's footprint in clothing goods.

What Amazon teaches us about business quality

My key takeaways from studying Amazon:

Amazon solved a real problem and genuinely improved the customer experience. Strategy mattered: one primary focus (customer obsession) executed relentlessly over decades.

Market cycles are important. Despite being a great business, Amazon's valuation fell 90% during the dot-com crash. The timing of your investment matters, and the same company operating in different market conditions can command very different valuations.

Investing in growth works if backed by revenue growth. Amazon never stopped investing in its ecosystem, and investors rewarded it.

The open ecosystem was the decisive strategic move. Turning competitors into partners and building an ecosystem rather than just a company created a moat that is nearly impossible to replicate.

M&A to drive further growth - Once it reached critical mass, Amazon flexed its financial power and began an aggressive M&A strategy to buy out competitors, expand into other sectors and grow its existing business.

Amazon ticks the three boxes I look for in long-term structural growth companies: a large and growing addressable market, a best-in-class product, and a favourable competitive position.